- Trading

- Trading

- Markets

- Markets

- Platforms

- Platforms

- Platforms

- Platforms

- Education

- Education

- Education

- Education

- Help & support

- Help & support

- About

- Trading

- Trading

- Markets

- Markets

- Platforms

- Platforms

- Platforms

- Platforms

- Education

- Education

- Education

- Education

- Help & support

- Help & support

- About

- Democrats might engage in impeachment procedures.

- There might be a reduction in policy changes.

- Tax reforms might change.

- Confidence will be affected following the escalation of trade tensions.

- There are still uncertainties around Brexit.

- Sources of risk outside the EU have grown.

News & Analysis

News & AnalysisUS Mid-Election & The Fed sticks to the Game Plan

9 November 2018

The propaganda around the US mid-election dominated the markets this week. With the Democrats now in control of the House of Representatives, the Congress will be tied up in a legislative gridlock leaving the market participants to evaluate the effects of the election results on the policy making in the US. As widely expected, the Democrats are empowered with investigative and procedural authorities, talks of “impeachment” are also unfolding.

The week will end with some notable data from the UK and second-tier economic releases from the US.

Equity Markets

After a rout in the equity markets in October, investors were waiting for the US mid-term elections to drive the markets. A significant uncertainty overshadowing equity was eliminated given that the outcome of the election is known. A divided Congress is not uncommon, but this time, the consequences might be substantial given that the Democrats are dealing with probably the most controversial and unconventional President.

Wall Street and the broader equity markets cheered up the outcome even though it could weigh negatively on the equity markets:

However, the relief rally was slightly dampened following the Federal Reserve’s statement. There were no signs that the Fed will be changing its plan for December and the markets are still pricing a 95% probability of a rate hike next month. Household spending and the housing sector are still supportive of the US economic growth, but the dovish undertone of the Fed regarding business spending raised concerns that a divided Congress will accentuate investors’ and business confidence. The Asian and European markets were also mostly driven by the same focus on the election results this week.

Investors will likely be driven by various policy bets which will be caught in a tussle between two parties. Investors will have to analyse the sectors that will outperform compared to the ones that will underperform as a result of the election results.

Generally, it will be a volatile environment for equities but not necessarily negative or bearish.

Currencies Markets

The price action in the FX markets was also revolved around a divided Congress and the Fed’s statement. The US dollar started the week on the back foot ahead of the elections. There were concerns that there might be a fiscal tightening due to a deadlock or more government shutdown which have put pressure on the US dollar. However, traders were gearing up for the FOMC meeting which helped the greenback to find buyers. The prospect that the December hike will be maintained propelled the dollar higher across the board. Besides the politics, the US data continue to show strong growth momentum.

In Europe, the standoff between Italy and the EU continues as both sides are unable to overcome their differences over Italy’s budget. Earlier this week, Draghi flagged a couple of downside risks that are holding the shared currency from advancing higher:

The downfall remained somewhat cushioned as the Eurozone economy is still in broad-based expansion although growth is slightly weaker than expected. The labour market is also strong. Currently, EURUSD is trapped in a tug of war between buyers and sellers unable to make a firm move in any direction.

EURUSD (Daily Chart)

Source: GO MT4As Theresa may looks close to securing a deal with the EU, Brexit headlines remain the key dominant factor driving the Sterling pairs. The Irish border is the sizable challenge as the PM is not willing to accept a divided UK with two custom territories. On the data front, the RICS Housing Price Balance showed that house prices took a beating due to Brexit uncertainties. After an impressive recovery last week, the Pound is sinking. The GBPUSD pair dropped to 1.30 after reaching a high of 1.31242.

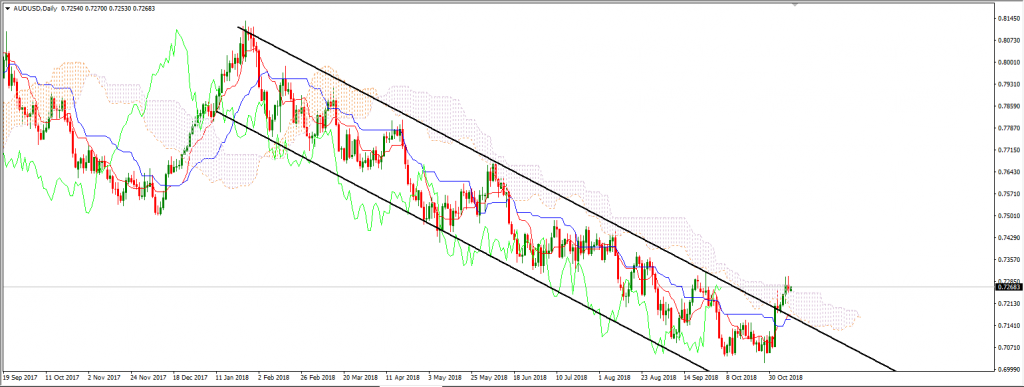

The Antipodeans are in the green against the US dollar for the week. The New Zealand dollar found support on strong jobs data which helped in lowering the probability of a rate cut. The Aussie dollar also rallied impressively to the upside, and AUDUSD even broke out of the bearish channel the pair was trapped in.

AUDUSD (Daily Chart)

Source: GO MT4Commodities Markets

The oil markets tumbled driven primarily by market forces. The rally in oil prices was attributed to fears that have grasped the markets but have since eased. Reports this week have shown a rise in the crude output, and at this rate, the US is overtaking Russia and Saudi Arabia as the world’s largest crude producer. WTI dropped to 8-month low and is currently trading at $60.87 as of writing.

USOUSD (Hourly Chart)

Source: GO Mt4Gold struggled to find demand and pared gains made at the start of the month. The greenback has been weaker, but still, demand for safe-havens was dampened as the stock markets rallied.

Monday, 12 Nov 2018

Indicative Index Dividends

Dividends are in PointsASX200 WS30 US500 US2000 NDX100 CAC40 STOXX50 11.558 0 0 0 0 0 0 ESP35 ITA40 FTSE100 DAX30 HK50 JP225 INDIA50 0 0 0 0 13.713 0 0 The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

#Economy #Economics #Finance #MarketsNext Article

WTI in Bear Mode

Deteriorating demand and rising global output are the main factors that sent the WTI Crude into a bear market territory. There is a shift of sentiment in the oil markets. The US sanctions have been the primary influence behind the rally in oil prices, and now that fears have eased, fundamentals took over, and economic forces- demand and su...

November 9, 2018Read More >Previous Article

Tied In A Gridlock, Eyes Are Now On The FOMC Meeting!

The results of the US Mid-term election have been released and the Democrats took control of the House of Representatives, securing Washingto...

November 8, 2018Read More >

- Trading

- Trading

- Trading

- Markets

- Markets

- Products overview

- Forex

- Commodities

- Metals

- Indices

- Shares

- Cryptocurrencies

- Treasuries

- Platforms

- Platforms

- Platforms

- Platforms

- Platforms overview

- MetaTrader 4

- MetaTrader 5

- Education

- Education

- Education

- Education

- News & analysis

- Education Hub

- Economic calendar

- Help & support

- Help & support

- About